You can’t keep prices the same indefinitely, but raising them is always a gamble. Consumers can — and do — compare prices anywhere, anytime, on everything.

You can’t keep prices the same indefinitely, but raising them is always a gamble. Consumers can — and do — compare prices anywhere, anytime, on everything.

If your bottom line needs a boost, raising prices can definitely help — as long as you map out a strategy and avoid some common pitfalls.

Promote, Promote, Promote

When you’re ready to roll out the increase, plan to roll out some promotions and coupons at the same time to take the sting out of higher prices. The discounts will help keep your most cost-conscious consumers in the fold. Making discounts and coupons readily available establishes the perception that all your prices are reasonable, which may or may not be true.

If you’re concerned about promotions hurting your bottom line, don’t be. Not all of your customers will clip coupons or shop sales. Ideally, you’ll sell enough items at the higher price to raise the average sale. If that’s not happening, you can always give prices another nudge, although it’s better to go with one large increase than several small ones.

Cut Carefully

Another way to improve your financial picture is to cut costs. One common tactic is to keep the price the same but shrink the amount of product (e.g., a skinnier box of cereal or slimmer container of juice). But this can backfire. If customers discover the change and feel cheated, you could become the target of a social media campaign, which could turn out badly. You could end up with less business and a ruined reputation.

Get Creative

Thinking outside the box (rather than shrinking it) might provide some opportunities to increase revenue. For instance, you might be able to unbundle a popular product. You can actually lower the price of the basic item, then add additional charges for each bell and whistle.

Add Value

Big box stores and online shopping may help customers find lower prices, but there’s one thing they can’t do. They can’t give their customers the kind of service you can. That’s a value only small businesses can offer. If you do it right, it can help you weather a price increase.

Call us today for more tips on how to ensure you’re following business best practices, and let us help you keep your company in the black.

Send us an e-mail or call us today at 901-685-9411 to discuss your business needs with an experienced CPA. Or, request a free consultation online.

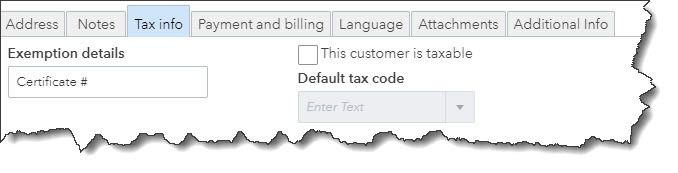

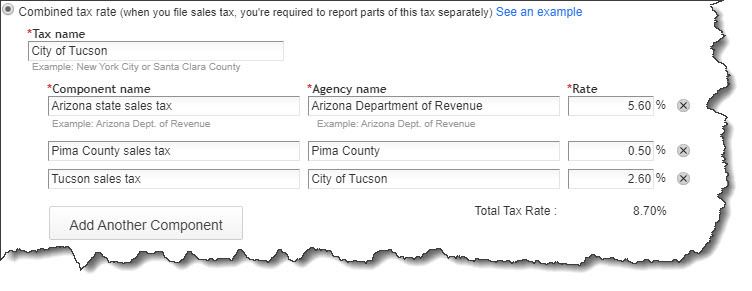

The most important thing you need to know about sales tax is that administering it correctly can be challenging.

The most important thing you need to know about sales tax is that administering it correctly can be challenging.

Launching a new business takes hard work — and money. Costs for market surveys, travel to line up potential distributors and suppliers, advertising, hiring employees, training, and other expenses incurred before a business is officially launched can add up to a substantial amount.

Launching a new business takes hard work — and money. Costs for market surveys, travel to line up potential distributors and suppliers, advertising, hiring employees, training, and other expenses incurred before a business is officially launched can add up to a substantial amount. Like many business owners, you may have structured your business as an S corporation because of the tax benefits it offers. An S corporation provides the same limited liability as a traditional C corporation, but it generally avoids the double taxation associated with a C corporation. You and the other shareholders (if any) pay income taxes on corporate income directly.

Like many business owners, you may have structured your business as an S corporation because of the tax benefits it offers. An S corporation provides the same limited liability as a traditional C corporation, but it generally avoids the double taxation associated with a C corporation. You and the other shareholders (if any) pay income taxes on corporate income directly. The federal spending package that was enacted in the waning days of 2019 contains numerous provisions that will impact both businesses and individuals. In addition to repealing three health care taxes and making changes to retirement plan rules, the legislation extends several expired tax provisions. Here is an overview of several of the more important provisions in the Taxpayer Certainty and Disaster Relief Act of 2019.

The federal spending package that was enacted in the waning days of 2019 contains numerous provisions that will impact both businesses and individuals. In addition to repealing three health care taxes and making changes to retirement plan rules, the legislation extends several expired tax provisions. Here is an overview of several of the more important provisions in the Taxpayer Certainty and Disaster Relief Act of 2019.